EVERYTHING YOU NEED TO KNOW…

CORPORATE TAX IN THE UAE: EVERYTHING YOU NEED TO KNOW

Background

With an aim to prevent harmful tax practise and to align with the international standards of tax transparency, the United Arab Emirates (UAE) Ministry of Finance (‘MoF’) has introduced Federal corporate tax in the UAE.

The UAE Corporate Tax (‘CT’) law will be effective for the financial years commencing on or after 01 June 2023 with a headline rate of 9%, one of the most competitive tax rates in the world. While certain clarifications are still awaited, the UAE MoF has released 158 Frequently Asked Questions which supplements the law and provide clarifications on the scope, applicability and various issues.

As a business owner, it is imperative to understand the tax laws and regulations in the country where one operates. Given the same, corporate tax would be a crucial aspect while doing business in the UAE.

In .this document, we have outlined the key features of the Corporate Tax in UAE law.

Key features of the Corporate Tax law in UAE

The Corporate Tax law in the UAE is a form of direct tax levied on the taxable income of the entity, which is arrived by making various tax adjustments to the net income or profit of corporations and other businesses of the entity.

Taxable persons

Residents in the UAE

- .Juridical Person (incorporated in UAE) including a Free Zone;

- .Natural persons conducting business in UAE;

- .Foreign Juridical person that are managed and controlled in UAE (POEM); and

- .Any other person as may be specified.

Non – residents

- .Permanent establishment in the UAE;

- .UAE sourced income; and

- .Nexus in the UAE (detailed clarification awaited).

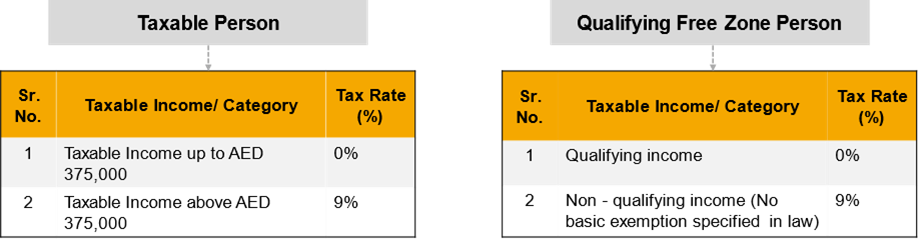

Corporate Tax Rates in the UAE

The following are the applicable corporate tax rates to various entities in the UAE:-

Tax period

The tax period shall be the financial year commencing on or after 01 June 2023.

Exempt person and Incentives

Following persons are exempt from the Corporate Tax in UAE law (subject to fulfilment of certain conditions) :-

- .Government entity;

- .Government controlled entity;

- .Person engaged in certain extractive business;

- .Person engaged in certain non-extractive natural resource business;

- .Certain qualifying investment funds;

- .Qualifying public benefit entity;

- .Pension or social security fund; and

- .Any other persons as may be specified in a decision issued by the Cabinet.

Small businesses with revenue below a certain threshold can claim ‘small business relief’ and be treated as having no taxable income during the relevant tax period and may be subject to simplified compliance obligations. To claim small business relief, an election must be made to the FTA.

The revenue threshold to qualify as ‘small business relief’ has not been specified yet and clarity would be provided with time by way of Cabinet Decisions.

Applicability to Free Zones:- In order to qualify for 0% Corporate Tax rate, Qualifying Free Zone Person shall meet all the following conditions:-

- .Maintains adequate substance in the UAE;

- .Derives Qualifying Income;

- .Has not elected to be subject to Corporate Tax In UAE;

- .Complies with all transfer pricing regulations; and

- .Meets any other conditions as may be prescribed by the MoF.

Conclusion

The tax payer needs to be mindful of the following :-

- .Review their activities and assess the impact of new Corporate Tax in UAE law on their business;

- .Consider readiness of their operations to manage the compliances and reporting obligations associated with the new Corporate Tax in UAE law; and

- .Maintain adequate documentation from Corporate Tax in UAE perspective.

FAQs

· Which industries are subject to corporate tax in the UAE?

All the entities in the UAE (except certain exempted entities) would be subject to corporate tax in the UAE.

· Are businesses in free zones exempt from corporate tax?

.Qualifying Income of a Qualifying Free Zone Person shall be taxed at 0% and the Non- Qualifying Income shall be taxable at 9%.

· Are there any incentives for businesses to invest in research and development in the UAE?

.From a corporate tax perspective, as of now, no separate incentives have been prescribed for businesses to invest in research and development in the UAE.

.What other taxes and regulations should businesses operating in the UAE be aware of?

Apart from Corporate tax laws, businesses in the UAE should be aware of indirect taxes, Economic Substance Regulation and Ultimate Beneficial owner regulations.

.How can businesses take advantage of the incentives offered by free zones in the UAE?

Businesses can obtain license from the relevant Free Zone authority and satisfy the prescribed conditions mentioned in Article 18 of the Corporate Tax in UAE law in order to take advantage of the exemptions and incentives offered.

.What impact does corporate tax have on foreign businesses operating in the UAE?

Foreign businesses shall be subject to the Corporate Tax in UAE, if they have a Permanent Establishment in the UAE or derives income from source in the UAE or has a nexus in the UAE as specified by the Ministry. Further, once the foreign businesses are covered by the Corporate Tax in UAE regime, they would be liable to get corporate tax registration, pay Corporate Tax in UAE on the taxable income in the UAE, comply with Corporate Tax in UAE compliances, maintain adequate documentation etc.

.Are there any penalties for not complying with corporate tax regulations in the UAE?

As of now, penalties for non-compliance with the Corporate Tax in UAE law have not been prescribed in the Corporate Tax in UAE law. We await a cabinet decision in this regard, specifying the provisions for penalties and prosecutions for non-compliance with the UAE Corporate Tax in UAE Law.

.Can businesses in UAE deduct expenses from their taxable income?

Article 28 to 33 of the Corporate Tax in UAe law contains provisions with respect to expenses that are deductible and non-deductible for Corporate Tax in UAE purpose.

It is important to keep accurate records of all expenses and consult with a tax professional to ensure proper deduction.

.How can businesses navigate the complex tax landscape in the UAE?

Businesses can seek professional advice from tax consultants, accountants, and legal advisors to navigate the complex tax landscape in the UAE. It is important to stay up-to-date on any changes to tax regulations and ensure compliance to avoid penalties and fines.

.Can businesses in the UAE carry forward losses to offset future tax liability?

Losses incurred prior to 01 June 2023 or prior to beginning of the first tax year, are not eligible to be set off against the income earned by the businesses. Further, losses incurred after the beginning of the first tax year are allowed to be set-off in the subsequent year to the extent of 75% of the year’s taxable income and remaining losses are allowed to be carried forward indefinitely.

.Is it possible for businesses in the UAE to claim tax treaty benefits?

Yes, businesses in the UAE can claim tax treaty benefits if there is a tax treaty between the UAE and the country in which the business is based. The tax treaty can help to reduce the tax liability of the business.

.What is the process for filing corporate tax returns in the UAE?

The tax payer shall be required to file Corporate Tax in UAE return online within 9 months from the end of the tax period.

Accounting Services

We at “MBA” believe that information is money…

Auditing Services

An independent audit is a foundation for decision-making in capital markets..

Vat in UAE

Value Added Tax or VAT is a form of indirect tax imposed on the use or…

Excise Tax Advisory Services

The introduction of excise tax in the UAE in 2017, every single…

Looking for help! Do not hesitate to contact us

Designed by Rock Media